For years, Elon Musk treated the public stock market like an infectious biological hazard. He famously declared that SpaceX would never go public until human beings were regularly commuting to Mars for weekend getaways. Going public meant answering to predictable, suits-and-ties quarterly analysts who care more about boring GAAP operating margins than building a multi-planetary civilisation.

Then June 12, 2026 happened.

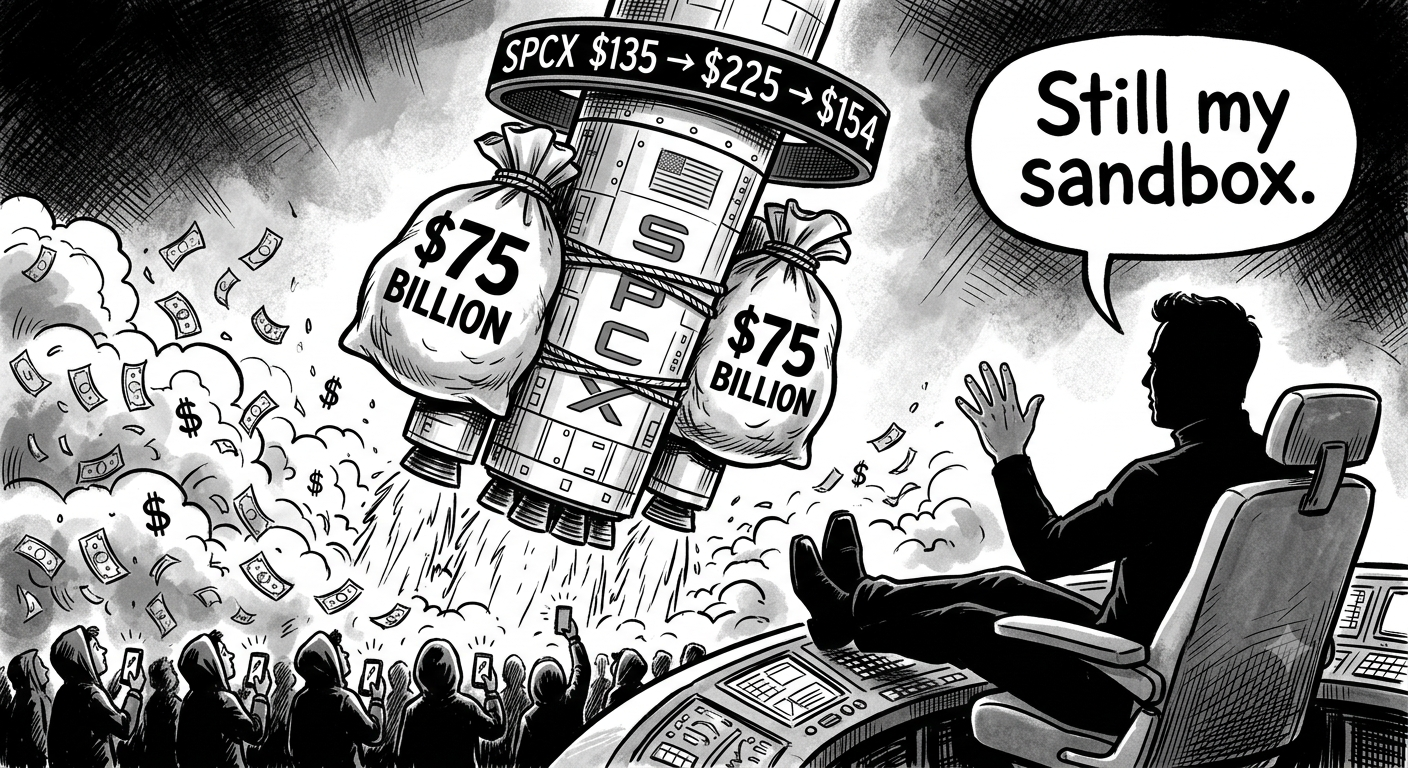

In an act of supreme financial theatre, SpaceX dropped the largest Initial Public Offering in the history of human capitalism. They didn't just cross the Karman line; they strapped a Falcon Heavy booster to the concept of public listings, raising a cool $75 billion by pricing 555 million shares at $135 each. The company swaggered onto NASDAQ under the ticker SPCX with a brain-melting initial valuation of $1.77 trillion.

Why the sudden 180-degree pivot from private sovereign fiefdom to public market board darling? Let's check the instruments in the cockpit.

1. Why Go Public Now? The xAI Ingestion & The Debt Bridge

The romantic narrative says Elon needs Grandma's retirement fund to build geodetic domes on Mars. The forensic accounting reality in their S-1 disclosures suggests something much closer to earthbound gravity.

Back in February 2026, SpaceX completed a massive all-stock merger to absorb xAI, Musk's artificial intelligence venture, valuing the private entity at an absolute premium. While SpaceX's core rocket launch services actually operated at a multi-billion-dollar deficit — logging a $4.9 billion net loss in fiscal 2025 — its Starlink connectivity segment was acting as the company's internal ATM, throwing off $4.4 billion in operating income.

But feeding Nvidia GPUs requires ungodly amounts of cash. SpaceX's IPO was a cosmic liquidity event designed to clear terrestrial balance sheet liabilities and bankroll a staggering $20.7 billion annual CapEx.

Best of all, thanks to a dual-class share structure, Elon retains absolute, undiluted voting power. He gets the public's $75 billion, uses it to lubricate his tech empire's gears, and still runs the cockpit exactly like his personal sandbox.

Masterful.

2. The Greenshoe Illusion & The Honeymoon Deflation

The IPO was structured beautifully to orchestrate a retail feeding frenzy. Underwriters handed everyday retail day-traders an unprecedented 30% allocation pool via apps like Robinhood. Naturally, the stock pulled a vertical ascent on day one, closing at $161 and eventually peaking at an intraday high of $225.64 as retail investors aggressively bought the top. The underwriters happily exercised their massive 83.3 million share greenshoe overallotment option to satisfy the hysteria.

But the financial honeymoon suffered a violent decompression.

Just days later, on June 22, SpaceX shocked its new public fan club by launching a surprise investment-grade senior unsecured notes offering. Wall Street instantly realised that SpaceX's cash burn is a literal black hole — their $20.7 billion CapEx completely swallowed their $18.7 billion in full-year revenue. The stock took a savage 16% single-day nose-dive, tumbling down to $154.60.

It's still above the $135 launch price, but the retail speculators who bought the peak are currently experiencing financial zero-gravity.

3. The Option Millionaires: Golden Handcuffs in Orbit

Inside the Hawthorne and Starbase facilities, thousands of engineers are furiously refreshing their portfolio trackers. SpaceX spent over a decade conducting tightly controlled internal secondary liquidity tranches — their employee option pool was already a finely tuned wealth-generation engine.

With the public market validating a multi-trillion-dollar peak valuation, thousands of mid-tier engineers became overnight millionaires. However, this creates an operational hazard. When a hardware genius responsible for the structural integrity of a 390-foot stainless steel Starship booster suddenly finds $5 million in their account, he might decide to leave the 90-hour weeks in the dusty Texas sun for a well-deserved Florida retirement.

Expect some highly creative, legally binding "retention lockups" to keep the talent from drifting off the pad.

4. The Data Centre in Space: Another Scientific Wet Dream?

Right before the listing dropped, Elon unveiled his ultimate narrative masterpiece: the space-based AI data centre cluster. The pitch was majestic — terrestrial data centres are running out of land, killing local power grids, and drinking rivers of water for cooling. So why not bolt compute racks directly onto Starlink V3 satellites, use the absolute zero of vacuum to cool the chips, and power them with giant solar arrays?

Is it a scientific wet dream? Mechanically, cosmic radiation degrades processing silicon at a terrifying rate, and shooting heavy servers into low Earth orbit is exponentially more expensive than plugging them into Ohio.

But narratively? It is absolute genius. By rebranding SpaceX from a "heavy industrial rocket company" into the ultimate orbital fabric for AI infrastructure, Musk successfully justified a tech-giant valuation multiple rather than a capital-heavy defence contractor multiple.

Genius.

5. Meanwhile — The Heavy-Metal Lords Are Laughing

When all the IPO fanfare has settled, the unglamorous infrastructure titans building the physical, terrestrial foundations that code and satellites actually rely on are quietly laughing all the way to the vault.

The Silicon Overlords (TSMC & ASML): It doesn't matter if an AI chip is deployed in a server farm in Memphis or bolted onto a Starlink satellite — it must be etched using ASML's extreme ultraviolet lithography systems and fabricated by TSMC. They hold the ultimate toll booth on advanced compute.

The Power Grid Monopolies (Eaton & Schneider Electric): Massive AI clusters require industrial-grade transformers, switchgears, and heavy distribution architecture. These legacy manufacturers are booking out backlogs years in advance, casually dictating terms to desperate tech giants waiting for power.

The Thermodynamic Kings (Vertiv): The terrifying heat generated by high-density AI nodes cannot be managed by a couple of desk fans. Liquid cooling is mandatory. Vertiv sits comfortably at the top of the supply chain, selling the literal plumbing that prevents the AI revolution from melting into slag.

The software kids got to play wizard with their text prompts for a while. But the heavy-metal lords of hardware just stood by the blueprints, waiting to hand them the bill for the plumbing.

Insidious.

"Insufficient facts always invite danger."

— Spock, Star Trek: The Original Series

The SpaceX IPO was priced at $135 a share on a $75 billion valuation. There were no public financials. No audited revenue figures. No disclosed profit margins. No breakdown of what Starlink actually earns versus what Falcon 9 costs to launch. Wall Street was handed a story, a charismatic founder, and an order book full of institutional FOMO — and told to figure out the rest themselves.

Spock would not have bought the dip.

Public Verified References

[1] Space Exploration Technologies Corp. (SPCX) NASDAQ Market Data — Post-listing historical data from June 12, 2026 through June 22, 2026, tracking IPO launch price ($135), peak intraday pricing ($225.64), and post-bond close ($154.60).

[2] S-1 SEC Prospectus & Financial Disclosures (May–June 2026) — Official financial metrics detailing SpaceX's fiscal 2025 operational performance, including $18.7B total revenue, $4.9B net loss, $20.7B CapEx, and Starlink/Connectivity segment income.

[3] Institutional Market Action Reports (June 23, 2026) — Documentation of the June 22 single-day market cap retraction following SpaceX's announcement of its investment-grade senior unsecured notes offering.

[4] Corporate Merger & Underwriting Allocation Filings (June 2026) — Details on the 30% retail allocation structure, the xAI merger completed in February 2026, and the execution of the 83.3 million share greenshoe overallotment option.

Note to the Lawyers: This is satirical commentary. All financial data is sourced from public SEC filings, NASDAQ market data and institutional reports. "Infinite money loop" and "personal sandbox" are editorial opinions, not legal characterisations. Not investment advice. If you bought SPCX at $225, Bearpanda is sorry — but Spock did warn you.