Palantir Technologies Inc. arrives in the boardroom like a benevolent wizard bearing gifts, promising to transmute your messy, chaotic data into pure, structured gold.

Seriously, what the batshit is an 'ontology' anyway, other than a tax on people who don't know how to write a SQL query? It's the ultimate piece of corporate theatrics — a high-signal grift masquerading as enlightenment.

Let me claw this:

The "Ontology" as a Soul-Binder

CEO Alex Karp famously declared that the idea of shorting "chips and ontology" is "batshit crazy," framing these components as the indispensable backbone of the modern AI stack. Yet, Palantir has convinced the C-suite that their software is the only way to navigate the corporate abyss. They aren't just selling a dashboard. In exchange for your autonomy over your data, you are gifted god-mode visibility. This is the Faustian bargain. You think you're the main character, but in reality you've just trapped your entire data in a proprietary loop where the "Architect" (or Grand Wizard) decides your reality.

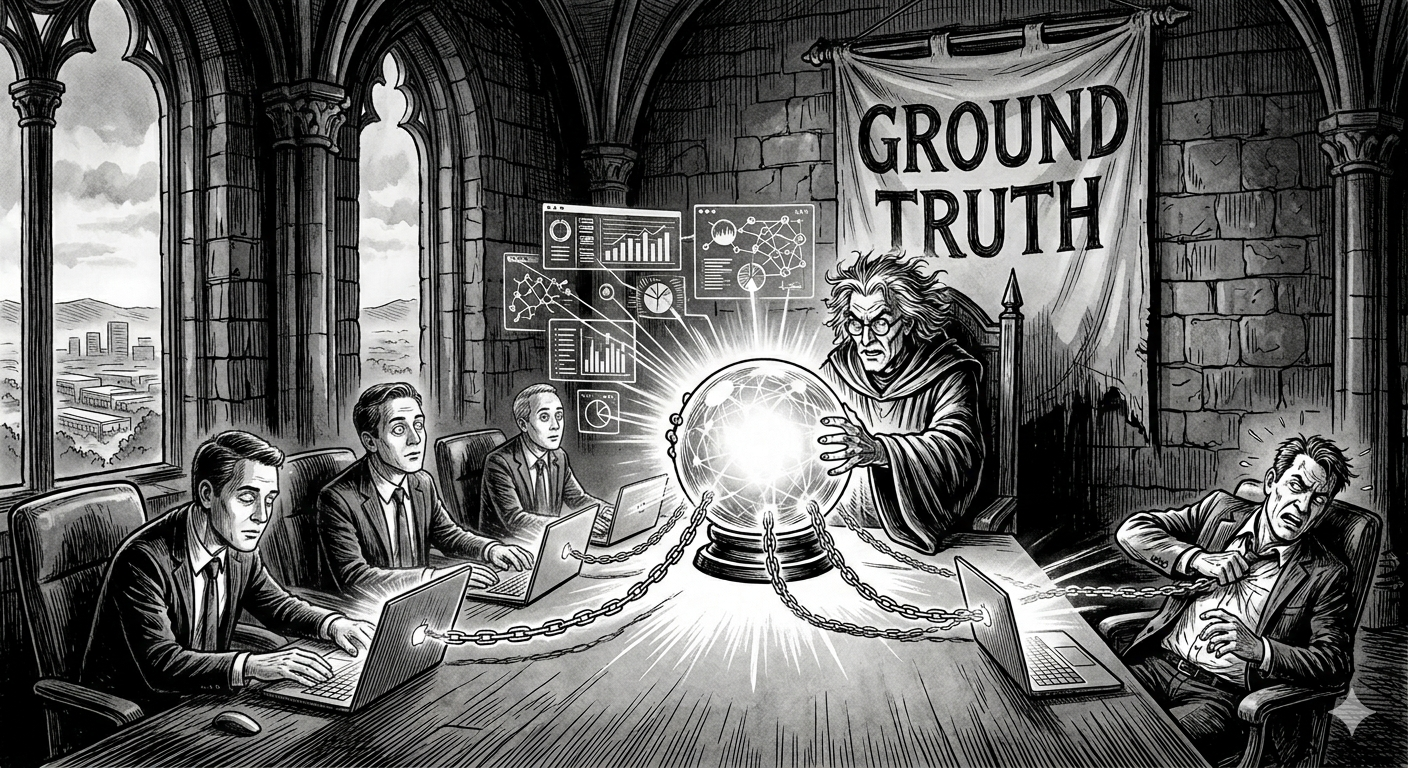

The Illusion of "Ground Truth"

Palantir loves to cite battlefield successes in Ukraine and beyond as proof of their "ground truth". Look behind the curtain, though. Their Q1 2026 earnings report shows massive growth — revenue up 85% year-over-year — but this is driven by aggressive U.S. commercial expansion and government spending, not magic. Palantir provides the shell, but the actual "transformational" work is just users hacking the system to work for their own dirty, real-world constraints.

Semantic Theatre in the Age of Hallucination

In 2026, as the industry grapples with LLM hallucinations, vendors are scrambling to rebrand metadata as "ontology" — so they can justify charging a premium for "grounding". Palantir is the lead actor in this theatre. By selling "constraints" as "intelligence," they maintain a narrative that the only way to avoid institutional collapse is to outsource your "ground truth" to their servers.

Not Everyone Buys into the Magic

Despite maintaining a GAAP net income margin of 53% and raising full-year 2026 revenue guidance to over $7.6 billion, the market remains deeply conflicted. While some maintain aggressive price targets, others argue that with an exit P/E multiple over 114x, the stock's valuation is largely priced for perfection, leaving it vulnerable to any deceleration in the AI narrative.

"A palantír is a dangerous tool, Saruman."

"Why? Why should we fear to use it?"

"They are not all accounted for, the lost Seeing Stones. We do not know who else may be watching!"

— Gandalf to Saruman, The Lord of the Rings · ▶ Watch the scene

The Bottom Line: Palantir isn't just selling software. It's selling a permanent reliance on a very specific way of seeing the world. The pitch to the CEOs is always the same: your business is too broken to fix itself, so let us build your reality for you.

It's a brilliant strategy — if you have a high tolerance for being permanently tethered to the Grand Wizard's "ontology."

Sources

[1] Palantir Technologies Q1 2026 Financial Results and SEC Filings.

[2] "The idea that chips and ontology is what you want to short is batsh*t crazy" — Alex Karp, 2025.

[3] Analysis of Palantir's valuation, P/E multiples, and market sentiment, 2026.

Note to the Lawyers: This is satire and critical commentary. If you think this is financial advice, you've already made a bigger mistake than anyone who bought PLTR at 114x earnings. All data is sourced from public filings and statements.